ou may have spent years running your veterinary practice, paying down debt and steadily improving your purpose-built clinic located in a desirable area, so it’s reasonable to think it would have increased in value over time. However, the economics of veterinary real estate don’t follow the logic of homeownership, or even general commercial retail…

Properties are primarily valued as income-generating assets—not simply as reflections of a building’s quality or location. Although those factors can influence the cap rate applied to those cash flows, appraisers and investors focus first on the lease structure, rent payments, tenant credit and perceived stability of income.

In fact, a practice operating out of a pristine, newly constructed clinic with below-market rent and an individual veterinarian or small group as the tenant may be valued lower than a nondescript box occupied by a national veterinary group with eight years left on the lease.

This catches many practice owners off guard when they begin preparing to divest their property or move onto a new chapter in their lives, and it leads to unrealistic expectations or strategic mistakes. Before you view your building as a financial windfall, you must see it for what it actually is.

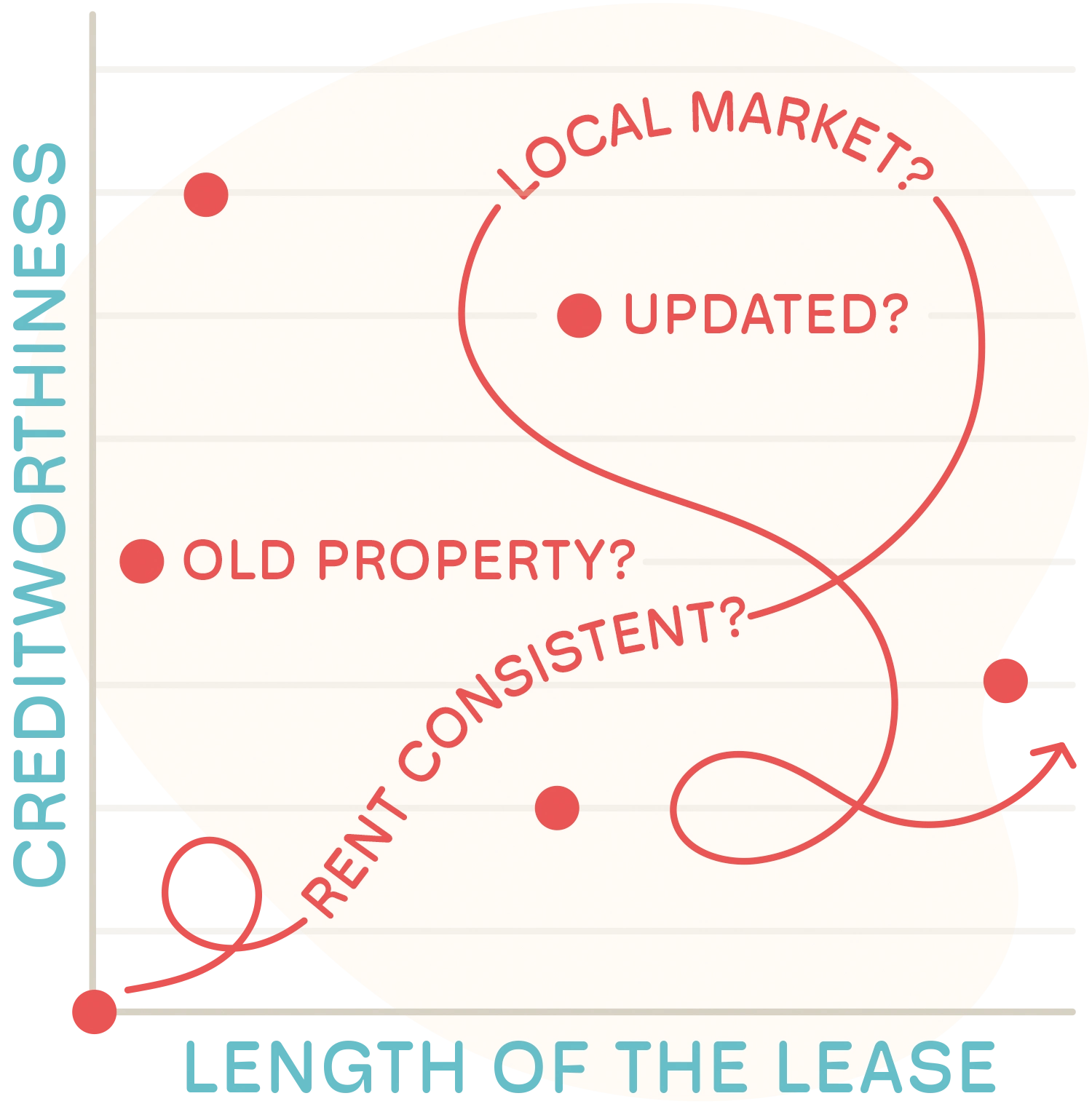

Another factor that can move value up or down is whether the rent in your lease matches the local market. Rates that stray far above or below the going rate—a common outcome when you own and operate your practice—can undercut value, as appraisers and buyers may adjust their figures to what a replacement tenant would realistically pay.

Older properties with long-term leases and high-credit tenants can appraise higher than newer ones with below-market rent or a short lease remaining for this reason. It’s counterintuitive, but it’s consistent.

But the lease itself can erode value, too. Some triple-net leases don’t always shift every responsibility to the tenant. If you’re on the hook for liabilities like HVAC maintenance or roof repairs, they reduce net income and lower the property’s appraised value. Making improvements may not translate into a higher sale price.

If a buyer finds your lease appealing, the focus shifts to whether the building can support the future of veterinary care.

One of the most common blind spots in veterinary real estate is the assumption that what works today will still work when it’s time to sell.

Some owners overbuild, while others underinvest. Large, high-spec clinics that never reach capacity can weigh down the business through rent or debt service. Underbuilt spaces with layout problems may make it harder for a buyer to envision continued growth.

Your practice’s performance matters, too. A lease with a financially strong tenant still carries risk if the economics don’t hold. Coverage ratios—especially EBITDA to rent—help buyers assess whether the economics work.

Recruiting and retaining talent is also part of keeping a practice performing well, yet clinicians may not be attracted to an outdated building. Although facilities converted from houses were once seen as charming, they’re losing appeal as younger veterinarians look for more professional, purpose-built environments. In addition, pet owners who consider their animals to be part of their family want clinics that feel like human medical facilities.

If those challenges raise questions about your building, a relocation may strengthen your financial position and simplify your exit when the time comes. Buyers are finding value in vacant drugstores, bank branches and other commercial spaces that have been repurposed into veterinary clinics. These second-use buildings may lease below replacement cost and offer you better parking, visibility and square footage than new construction.

It’s real estate, so location still matters a lot. The more your property is aligned with what buyers want next—and not just what you’ve needed—the more value you’ll have when the time comes to sell.

Just remember that external factors like interest rates, insurance shifts and labor dynamics will also affect how your property is priced. You don’t need to think like an investor, but it helps to see what investors see—because that lens can help you get more from the building you already have.